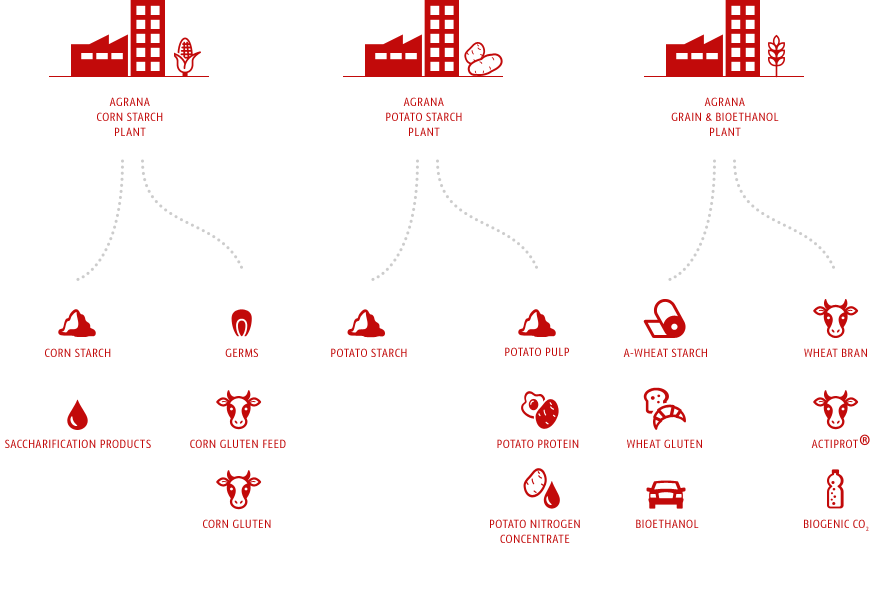

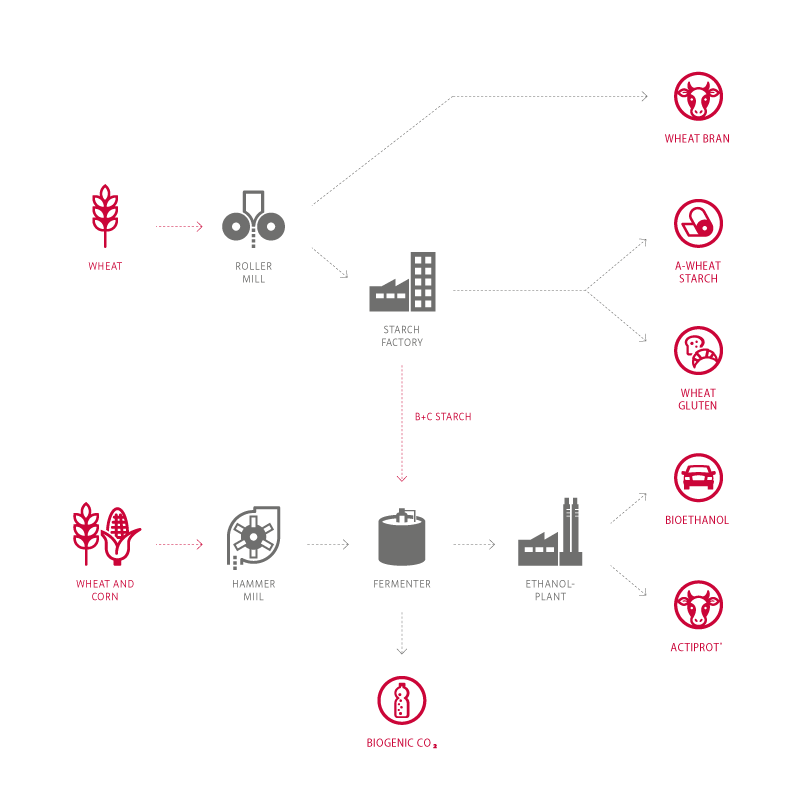

| Marketing relationshipB2B | ProductsGeneral division into food, non-food and feed sectors; Native and modified starches, saccharification products, alcohols/bio-ethanol, by-products (feedstuffs and fertilisers) | Raw materials processedCorn (maize), wheat, potatoes |

| Key marketsCentral and Eastern Europe, principally Austria and Germany; also specialty markets, e. g., in USA and UAE | CustomersFood sector: food industry; Non-food sector: paper, textile, construction chemicals, pharmaceutical, cosmetics and petroleum industries; Feed sector: feed industry | Special strengthsGMO-free and strong organic focus |

Revenue in the Starch segment grew substantially in the 2022|23 financial year, by 28.0% to € 1,293.8 million. The extreme increases in raw material and energy prices led to significantly higher manufacturing costs, which AGRANA was partly able to pass on in sales prices. The revenue growth was thus price-driven, and this was the case across the entire portfolio. In the ethanol business, sales prices are based on the Platts quotations. The volatility in ethanol markets seen in the last financial year was extreme. After quoting as high as above € 1,300 per cubic metre in the first half of 2022|23, ethanol prices fell significantly from the end of summer 2022 and only ranged between € 700 and € 800 per cubic metre since November 2022. By-product sales revenue (notably in high-protein products) increased significantly, following raw material prices higher. The high general level of prices moderated demand and sales volumes thus eased evenly across all product groups.The Starch segment’s share of Group revenue was 35.6% (prior year: 34.8%).

With EBIT of € 80.2 million, the Starch segment’s operating profit surpassed that of the previous year by 11.9%. A very good performance reflected in this was that of the wheat gluten business. Margins on the core products declined due to the significant uptrend in raw material and energy prices. The earnings contribution by the equity-accounted HUNGRANA group declined from € 13.8 million to € 11.0 million. Historic high corn prices in Hungary (due in part to local crop failures) and the increased energy prices were factors detracting from the result of this Hungarian joint venture, particularly in its ethanol business. On balance, the EBIT profit margin of the Starch segment in 2022|23 eased to 6.2%, from 7.1% in the prior year.

In the 2022|23 financial year, the COVID-19 pandemic, which had dominated world and economic events for the two previous years, moved to the background. It was eclipsed by the outbreak of war in Ukraine in late February 2022, which wrought dramatic and lasting changes in the economic environment.

Raw material and energy costs reached unprecedented levels, which for the first time required current annual contracts with customers to be revisited intra-year. In very demanding, but constructive, rounds of negotiations, the goal was to pass on cost increases as best as possible. As well, the use of shorter contract terms and the desire of many customers to stock up as early as they could for the coming year were factors determining market behaviour across all product segments.

At the beginning of the financial year, all product categories were in high demand by the market. In some categories, such as spray-dried saccharification products, limited availability meant that demand could only partly be met. Sales volumes of native and modified starches in the food sector and of proteins were high, with gratifying volume growth recorded particularly in specialties and organics. At the beginning of the financial year, the paper industry too had a very good order situation and thus strongly stimulated demand for cereal starches.

In the course of the year, however, the spike in energy prices led to the first, in some cases significant, declines in market demand. Due to the explosion in energy costs, customers in the paper sector were the first to be confronted with a loss of competitiveness in export markets. Towards the end of the financial year, this trend expanded to the whole starch market and the progressively weaker demand collided with improved availabilities; for example, new capacity in Southeastern Europe created local overcapacity in the market.

In the market for infant formula, almost all well-known European manufacturers suffered from overcapacity, due above all to the restrictions in supplying the Asian market. However, AGRANA’s focus on premium products enabled it to achieve nearly stable sales volumes in this market segment.

Volatility in the fuel alcohol market remains high. After strong quotations especially in the first quarter of 2022|23, the alcohol business was a key profit source for the Starch segment until the end of the first half of the financial year. However, high prices for energy and raw materials were exerting continuous heavy pressure on the cost side. In addition, ethanol prices in Europe fell significantly since the end of summer 2022, the top reason being the considerable amount of imports, particularly from Brazil and the USA. Forward prices for ethanol for 2023 have also declined accordingly. The food vs feed vs fuel debate that arose in the course of the grain price rally eased again, since an energy crisis in Europe not only appeared more likely than a food crisis but did, in fact, come to pass.

The EU’s Renewable Energy Directive (RED II), adopted in December 2018, has material significance for the business activities of the Starch segment. This directive also sets the target values for the time horizon of 2021 to 2030. It was transposed into national law through an amendment to Austria’s 2012 Fuel Regulation published on 13 December 2022 that came into force on 1 January 2023. It sets a GHG reduction target of 13% by 2030. The introduction of E10 in Austria is seen as a key option for achieving this reduction target. At the time of this reporting, the implementation of RED III, through which the use of renewable energy is to be increased and greenhouse gas emissions reduced, was being negotiated in the European and national bodies.

The EU decision in October 2022 to end new registrations of vehicles with internal combustion engines as of 2035 was noted by AGRANA, but according to current assessments does not pose a relevant risk to bioethanol production. First of all, bioethanol is only one of several products under the circular economy concept of the biorefinery in Pischelsdorf, Austria. Moreover, amid the phase-out of fossil products, bioethanol will find uses beyond that in fuels.

World grain production1 in the 2022|23 grain marketing year (1 July to 30 June) is estimated by the International Grains Council (IGC) at 2.248 billion tonnes (prior year: 2.291 billion tonnes), which is below the previous year’s level and also less than the expected consumption of 2.266 billion tonnes. Global wheat production is forecast at 796 million tonnes (prior year: 781 million tonnes), barely exceeding expected consumption of 789 million tonnes (prior year: 783 million tonnes). The world’s corn production is projected at 1,153 million tonnes (prior year: 1,220 million tonnes) and the predicted consumption of corn is 1,180 million tonnes (prior year: 1,217 million tonnes). Total ending grain stocks, at 597 million tonnes, are estimated to fall about 19 million tonnes short of the year-earlier amount.

Grain futures prices were marked by strong volatility throughout the financial year, buffeted by war-driven turmoil and unfavourable weather conditions. Quotations for corn and wheat on the Euronext Paris commodity derivative exchange initially rose sharply in the first months of the financial year, following the outbreak of the war in Ukraine. Since summer 2022, a falling trend could be seen. The price declines on the exchanges were caused by lower demand, an absence of further escalations of the war, agreed export corridors from Ukraine, and large harvests in important production regions. At the balance sheet date of 28 February 2023, on Euronext Paris, wheat quoted at € 274 per tonne and corn was at € 279 per tonne (year earlier: € 323 per tonne for wheat and € 311 for corn).

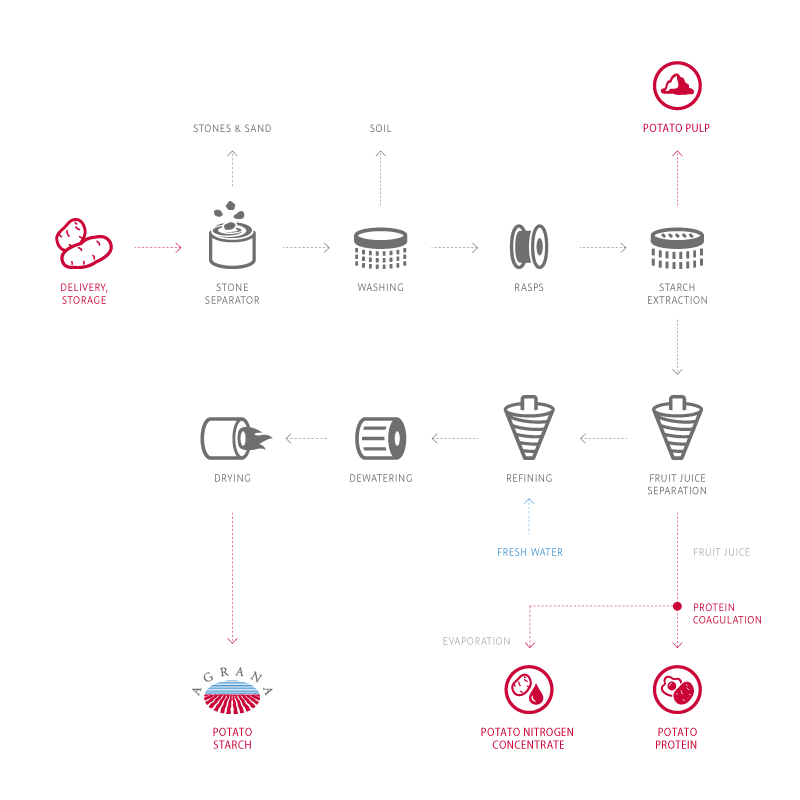

In the 2022|23 campaign, the potato starch factory in Gmünd, Austria, processed about 217,000 tonnes of starch potatoes (prior year: 274,000 tonnes). The processing of food potatoes for the production of long-life potato products was in line with the prior-year volume.

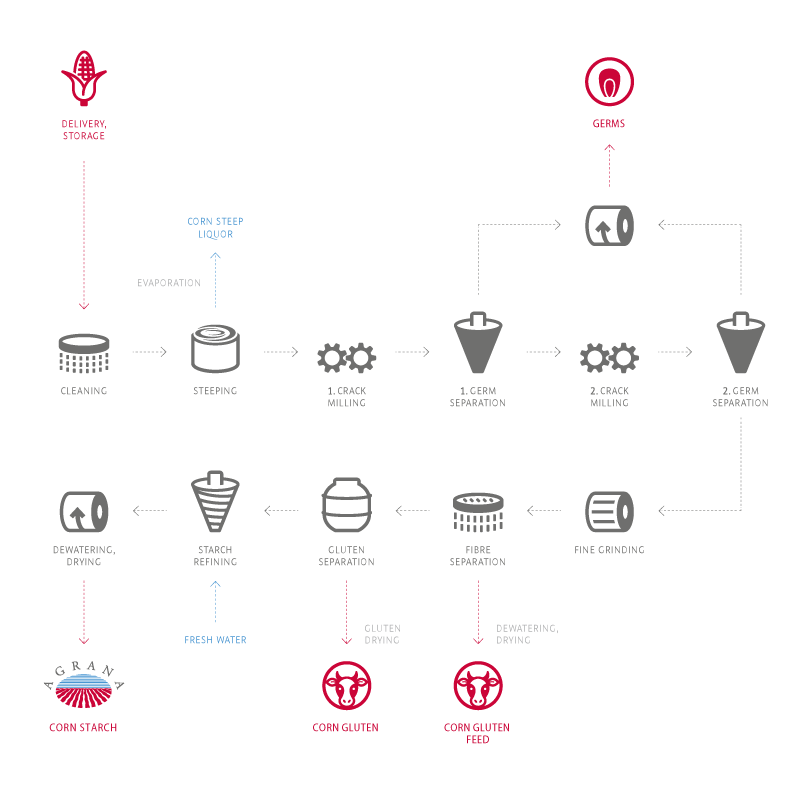

In 2022|23, AGRANA Stärke GmbH processed approximately 6% less corn at the Austrian sites in Aschach and Pischelsdorf than in the year before. The share of specialty corn (notably waxy corn and organic corn) was about 24%.

Wheat milling volume at the Pischelsdorf facility for the production of wheat starch and bioethanol was moderately lower in 2022|23 than in the previous year. Through delivery contracts concluded with growers in advance, AGRANA also secured ethanol wheat.

At the two Austrian locations, a total of about 1.4 million tonnes of corn and other cereals was processed in the financial year.

In 2022|23, the HUNGRANA facility in Hungary was not able to duplicate its grinding volume of the year before. The plant in Romania processed more specialty corn and less yellow corn than in the previous year.

1 IGC forecast of 16 February 2023.

The Starch segment invested € 31.0 million during the 2022|23 financial year (prior year: € 24.3 million). The following projects were carried out among others:

Additionally, € 20.9 million (prior year: € 14.1 million) was invested in 2022|23 in the HUNGRANA companies (amounts for these equity-accounted joint ventures are stated at 100% of the total).